The "huge story", as Graticule's Adam Levinson called it, will, it appears, be a "wake up call" for the West that seems to happily be ignoring this potential bombshell that is China's looming launch of domestic oil futures trading.

Additionally, Levison warns Washington that besides serving as a hedging tool for Chinese companies, the contract will aid a broader Chinese government agenda of increasing the use of the yuan in trade settlement... and thus the acceleration of de-dollarization and the rise of the Petro-Yuan.

“I don’t think there’s any doubt we’re going to see use of the renminbi in reserves go up substantially”

China has been planning this for a number of years and given rising tensions, now seems like a good time for China to flex a little.

The Shanghai International Energy Exchange, a unit of Shanghai Futures Exchange, will be known by the acronym INE and will allow Chinese buyers to lock in oil prices and pay in local currency. Also, foreign traders will be allowed to invest -- a first for China’s commodities markets -- because the exchange is registered in Shanghai’s free trade zone. Even Bloomberg admits there are implications for the U.S. dollar’s well-established role as the global currency of the oil market, as Sungwoo Park sums up some of the key questions...

- When will trading begin?

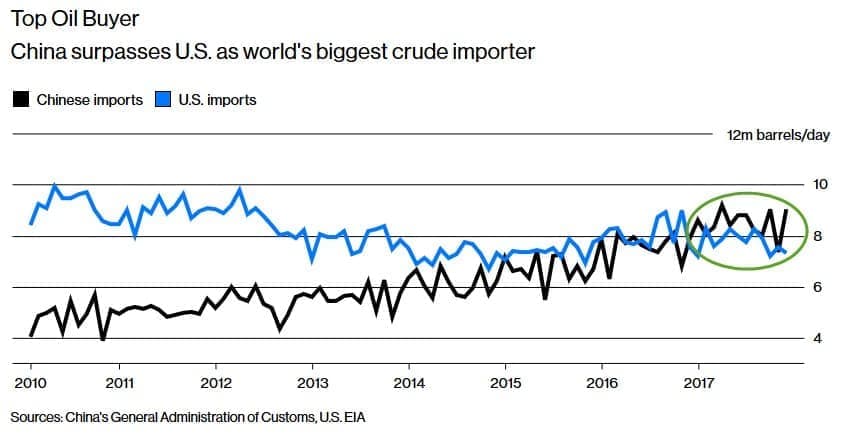

According to the Shanghai-based news portal Jiemian, which cited an unidentified person from a futures company, trading is expected to start Jan. 18. Multiple rounds of testing have been carried out and all listing requirements met. The State Council, China’s cabinet, was said to have given its approval in December, one of the final regulatory hurdles. The push for oil futures gained impetus in 2017 when China surpassed the U.S. as the world’s biggest crude importer.

- Why is this important for China?

Futures trading would wrest some control over pricing from the main international benchmarks, which are based on dollars. Denominating oil contracts in yuan would promote the use of China’s currency in global trade, one of the country’s key long-term goals. And China would benefit from having a benchmark that reflects the grades of oil that are mostly consumed by local refineries and differ from those underpinning Western contracts.

- How do oil futures work?

Futures contracts fix prices today for delivery at a later date. Consumers use them to protect against higher prices down the line; speculators use them to bet on where prices are headed. In 2017, oil futures contracts in New York and London outstripped physical trading by a factor of 23. Crude oil is among the most actively traded commodities, with two key benchmarks: West Texas Intermediate, or WTI, which trades on the New York Mercantile Exchange, and Brent crude, which trades on ICE Futures Europe in London.

- Why didn’t China begin trading futures until now?

Lower crude prices have played a part. Chinese oil futures were proposed in 2012 following spikes above $100 a barrel, but prices in 2017 have averaged little more than $50. There’s also concern over volatility. China introduced domestic crude futures in 1993, only to stop a year later because of volatility. In recent years, it repeatedly delayed its new contract amid turmoil in equities and financial markets. Such destabilizing moves have often prompted China’ government to intervene in markets in one way or another.

- What’s China’s track record in commodities?

Nickel was the last major commodity to be listed there in 2015; within six weeks, trading in Shanghai surpassed benchmark futures on the London Metal Exchange, or LME. In China, speculators play a far greater role, boosting trading volumes but making markets susceptible to volatility. In early 2016, the then-head of the LME said it was possible some Chinese traders did not even know what they were trading as investors piled into everything from steel reinforcement bars to iron ore. Steep price rises relented when China intervened with tighter trading rules, higher fees and shorter trading hours.

- Will foreigners buy Chinese oil futures?

That remains to be seen. Overseas oil producers and traders would need to swallow not just China’s penchant for occasional market interventions but also its capital controls. Restrictions on moving money in and out of the country have been tightened in the past two years after a shock devaluation of the yuan in 2015 prompted a surge in money leaving the mainland. Similar hurdles have kept foreign investors as bit players in China’s giant stock and bond markets.

- Could the yuan challenge the dollar’s dominance in oil?

Not any time soon, since paying for oil in dollars is an entrenched practice, according to some analysts. Shady Shaher, head of macro strategy at Dubai-based lender Emirates NBD PJSC, says it makes sense in the long run to look at transactions in yuan because China is a key market, but it will take years. Bloomberg Gadfly columnist David Fickling argues that China doesn’t have “nearly the influence in the oil market needed to carry out such a coup.” On the other hand, paying in yuan for oil could become part of President Xi Jinping’s "One Belt, One Road" initiative to develop ties across Eurasia, including the Middle East. Chinese participation in Saudi Aramco’s planned initial public offering could help sway Saudi opinion toward accepting yuan, which is used in only about 2 percent of global payments.

With regards that final point from Bloomberg, Pepe Escobar disagrees, recently concluding, the era of the petro-yuan is at hand...

Intractable questions referring to the US dollar as top reserve currency have been discussed at the highest levels of JP Morgan for at least five years now. There cannot be a more politically charged dossier. The NSS duly sidestepped it.

The current state of play is still all about the petrodollar system; since last year what used to be a key, “secret” informal deal between the US and the House of Saud is firmly in the public domain.

Even warriors in the Hindu Kush may now be aware of how oil and virtually all commodities must be traded in US dollars, and how these petrodollars are recycled into US Treasuries. Through this mechanism Washington has accumulated an astonishing $20 trillion in debt – and counting.

Vast populations all across MENA (Middle East-Northern Africa) also learned what happened when Iraq’s Saddam Hussein decided to sell oil in euros, or when Muammar Gaddafi planned to issue a pan-African gold dinar.

But now it’s China who’s entering the fray, following on plans set up way back in 2012. And the name of the game is oil-futures trading priced in yuan, with the yuan fully convertible into gold on the Shanghai and Hong Kong foreign exchange markets.

The Shanghai Futures Exchange and its subsidiary, the Shanghai International Energy Exchange (INE) have already run four production environment tests for crude oil futures. Operations were supposed to start at the end of 2017; but even if they start sometime in early 2018 the fundamentals are clear; this triple win (oil/yuan/gold) completely bypasses the US dollar.

The era of the petro-yuan is at hand.

Of course, there are questions on how Beijing will technically manage to set up a rival mark to Brent and WTI, or whether China’s capital controls will influence it. Beijing has been quite discreet on the triple win; the petro-yuan was not even mentioned in National Development and Reform Commission documents following the 19th CCP Congress last October.

What’s certain is that the BRICS supported the petro-yuan move at their summit in Xiamen, as diplomats confirmed to Asia Times. Venezuela is also on board. It’s crucial to remember that Russia is number two and Venezuela is number seven among the world’s Top Ten oil producers. Considering the pull of China’s economy, they may soon be joined by other producers.

Yao Wei, chief China economist at Societe Generale in Paris, goes straight to the point, remarking how “this contract has the potential to greatly help China’s push for yuan internationalization.”

It ain’t over till the fat (golden) lady sings. When the beginning of the end of the petrodollar system – established by Kissinger in tandem with the House of Saud way back in 1974 – becomes a fact on the ground, all eyes will be focused on the NSS counterpunch.

Source : oilprice.com